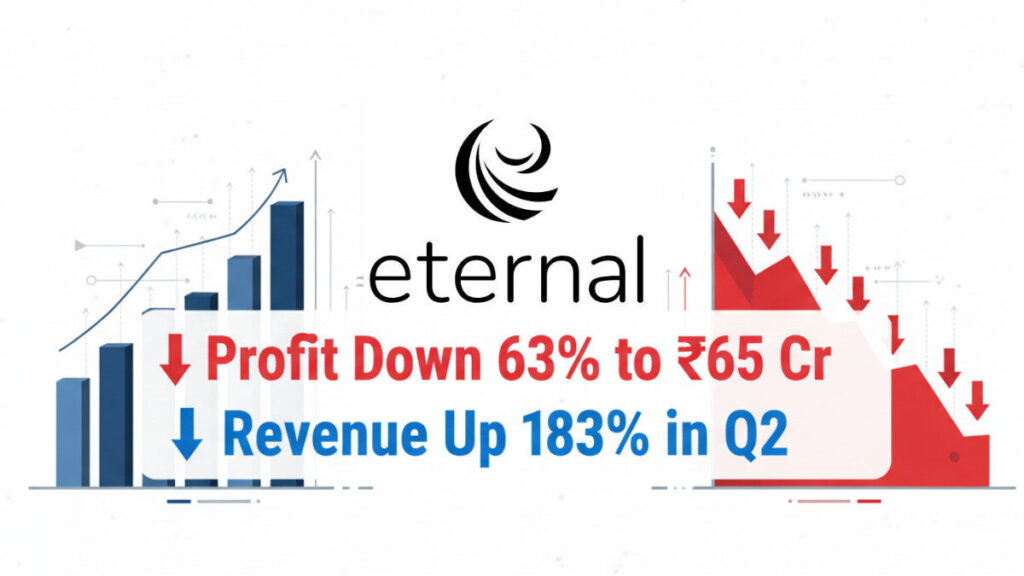

India-based fintech company Eternal has reported a 63% decline in net profit to ₹65 crore for the quarter ended September 2025 (Q2 FY26), even as its revenue jumped 183% year-on-year to ₹1,215 crore.

Strong Growth in Revenue, But Rising Costs Bite

Eternal’s impressive revenue growth was driven by the expansion of its lending and payment services business. However, higher operational costs, increased provisioning, and marketing spends weighed heavily on the company’s profitability.

The company’s operating expenses surged due to aggressive customer acquisition strategies and platform upgrades. Despite the short-term dip in profits, analysts view Eternal’s move as a long-term growth push aimed at strengthening its market position against fintech rivals.

Management’s Statement

Eternal’s spokesperson said, “Our revenue growth validates the strong demand for our financial services. We’re investing strategically to scale responsibly and ensure sustainable profitability in the coming quarters.”

Market Outlook

Experts believe that Eternal’s short-term profitability dip reflects its investment phase. With strong revenue momentum and expanding user base, the company is expected to rebound in the next few quarters if it controls costs effectively.

📊 Summary Table

| Particulars | Q2 FY26 | Q2 FY25 | YoY Change |

|---|---|---|---|

| Revenue | ₹1,215 crore | ₹429 crore | 🔼 183% |

| Net Profit | ₹65 crore | ₹175 crore | 🔻 63% |

| Operating Margin | 5.3% | 13.8% | ↓ |

| Key Growth Driver | Lending & Payments | — | — |